Data from the Nationwide House Price Index shows that UK house price growth eased in May 2020 for the first time since September last year. Despite the dramatic drop showed in our chart of the month, average annual house prices still continued to grow in May albeit at nearly half the April rate. It is worth noting that UK house prices had continued to gain strong momentum even after the lockdown was introduced, and in April climbed by 3.7% year-on-year, a three-year high. In May, UK house prices grew by 1.8% year-on-year taking the cumulative growth during the first five months of 2020 to 2.5% compared to last year. Not surprisingly, month-on-month growth in house prices entered into negative territory and indeed saw one of its steepest monthly declines since the record began in 1991.

Chart of the month: UK house price year % change

Source: Nationwide House Price Index

Market Commentary

- The Nationwide House Price Index shows that annual house price growth dropped to 1.8% in May, down from a nearly three-year high of 3.7% reached in April despite of the full-scale of the Covid19-related lockdown. Annual growth therefore remains positive and relatively strong compared to the trend seen over the past five years. Obviously monthly price growth was negative, and we saw one of the largest month-on-month declines in Nationwide’s series since it started in 1991.

- In the first five months of 2020, before the pandemic struck, the UK housing market had been steadily gathering very strong momentum and earlier data has even been revised upwards. Last month we reported that prices rose by 0.7% month-on-month in April, the second-strongest rate for 28 months, yet slightly lower than the 0.8% month-on-month growth seen in March. This number has now been revised upwards to 0.9% month-on-month in April, making it the strongest monthly growth since May 2015, and making the period up until April the longest period of sustained year-on-year price growth over the past five years. It is not surprising then that charts of decline in May appear very dramatic in the context of the previous strong growth.

- The impact of the slowdown on the data tends to show with a lag due to the way the Nationwide House Price Index is constructed: it uses mortgage approval data, and there is a lag between mortgage applications being submitted and approved. Therefore, we believe that the impact of pandemic in the housing data will continue to be seen in the June data. Indeed, recent data from HMRC showed that residential property transaction were down by 53% in April compared with the same month in 2019. The medium-term outlook for the UK housing market remains highly uncertain at this point and dependent on the wider economic performance. We are likely to see the full impact of the lockdown over the next few months as housing market activity effectively ground to a halt in April as a result of the measures implemented to control the spread of the virus.

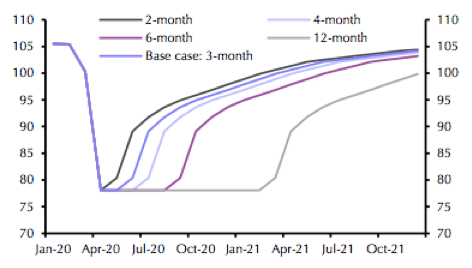

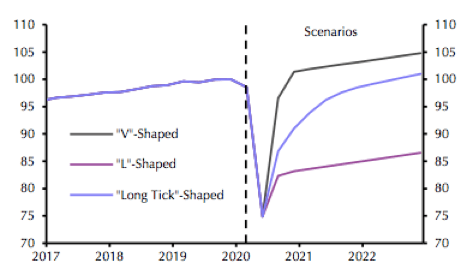

- Our Figures 1 & 2 this month show the different lockdown and recovery scenarios modelled by Capital Economics. Their basecase assumes a three-month period of stringent measures before a bounce back in activity during H2 2020 and into 2021. This translate into a “long tick” shaped recovery whereby activity recovers quickly as restrictions are eased but we will see increases in insolvencies and unemployment.

Figure 1: GDP Lockdown Scenarios (100 = 2016)

Source: Capital Economics

Figure 2: GDP Recovery Scenarios (100 = Q4 2019)

Source: Capital Economics

As you will have seen, we recently funded our two largest deals and also returned £2,282,000 to lenders on six loans. Our underwriting team at Blend Network remain very busy assessing deals to ensure we continue lending to experienced property developers who come to us with a solid project, an enviable track record and a strong exit strategy. We know you are hungry for more deals and ‘we’ve got them for you’! So, keep an eye for new loans coming at www.blendnetwork.com.

Your capital is at risk if you lend to businesses. P2P lending is not covered by the Financial Services Compensation Scheme. Investments are illiquid (the inability to sell assets quickly or without substantial loss in value). Past performance is not a reliable indicator of future results.

Blend Loan Network Limited is an Appointed Representative of Resolution Compliance Limited which is authorised and regulated by the Financial Conduct Authority (FRN. 574048)